$RMBS - 4/28/2026

| RMBS | $111.27 | -21.26% | -20.77 | 4.0x | Other / Small Cap |

The Wheel Candidate: RMBS — read the fine print

The screen suggests $95P @ $5.05 (Δ0.23, 38% annualized). But RMBS is also in the bearish momentum list at -21.26% today, and the email shows IV Rank as 0 which is almost certainly a data error after a 21% drop — IV should be elevated, hence the rich premium.

The setup itself isn't bad: $95 strike is ~15% below spot, 51 DTE gives time. The question is why it dropped 21%. Since it's not in the earnings movers section, this was news-driven (downgrade, guidance cut, lawsuit, etc.). Don't sell that put until you know the catalyst. If it's clean (downgrade only), the wheel works. If it's a fundamental impairment, you're catching falling knives at $95.

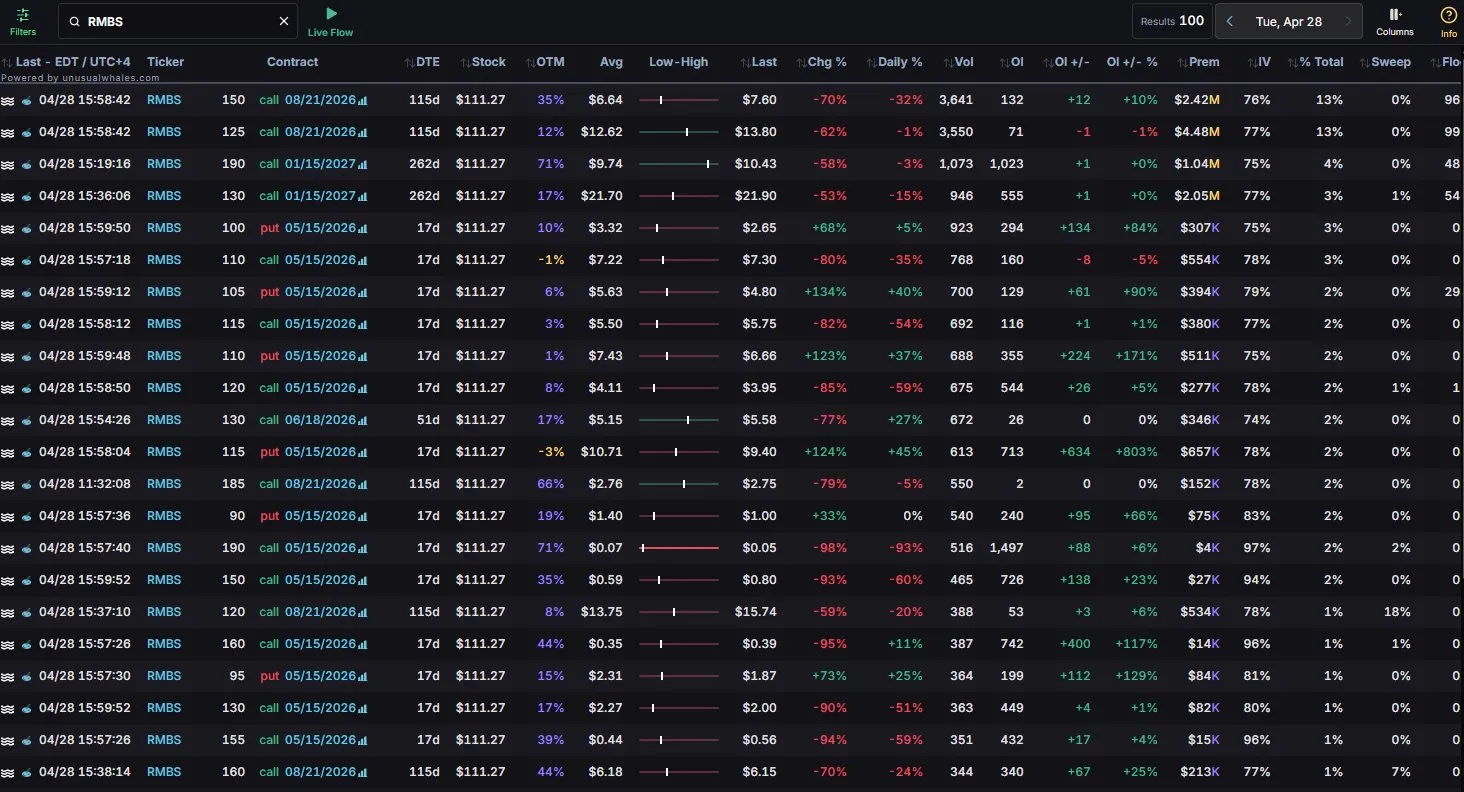

RMBS gapped down huge after a decent gap up two days ago. Here is the unusual whales scan.

The Backstory You Need

RMBS isn't a normal -21% drop — it's an unwind of an extraordinary run. RMBS nearly doubled from $79.73 on March 30 to a peak of $158.40 on April 24, driven by AI memory momentum. Then earnings landed Monday night and the floor came out today: TIKR

- Q1 revenue of $180.2M missed consensus of $189.71M; adjusted EPS of $0.63 was a hair below the $0.64 forecast. Yahoo Finance

- Baird downgraded from Outperform to Neutral, maintaining a $120 price target, citing softening product revenue momentum — Q2 product revenue guidance implies just 1% growth versus Q4 2025. Yahoo Finance

- A Wall Street analyst flagged that Rambus's business is less able to raise prices in memory shortages because it's leveraged to total units sold. The Motley Fool

The "gap up 2 days ago" you saw was the run into earnings. Today is the air coming out. Crucially: William Blair, Jefferies, and Rosenblatt all maintained Buy ratings — Rosenblatt has a $130 price target. Even the bearish Baird PT of $120 is above today's close. This isn't a broken company — it's a re-rated valuation. CoinCentral

What The Flow Actually Says

Forget the call activity — those are existing call holders puking on the close (volumes high, OI flat or down, premiums down 70-98%). The real signal is on the put side.

Massive new put OI build in the May 15 expiry (17 DTE):

| Strike | Premium | OI Change | OI % |

|---|---|---|---|

| $115P | $9.40 (+124%) | +634 | +803% |

| $110P | $6.66 (+123%) | +224 | +171% |

| $105P | $4.80 (+134%) | +61 | +90% |

| $100P | $2.65 (+68%) | +134 | +84% |

| $95P | $1.87 (+73%) | +112 | +129% |

| $90P | $1.00 (+33%) | +95 | +66% |

That's ~1,260 contracts of new put OI built end-of-day across the entire $90-$115 strike chain on a 17-day expiry. That spread of strikes — both ATM and well-OTM filling in together — is the signature of put debit spreads or put butterflies, not pure directional buys. Someone with size is paying up to position for further downside in the next 2-3 weeks, but capping their bet (which is why all the strikes light up rather than just one).

The $160C +400 OI on the May 15 chain is the only meaningful call open — at $0.39 it's a lottery ticket, not a thesis.

What This Means For The Wheel

The original scan recommended $95P 06/18/26 @ $5.05 (51 DTE, Δ0.23, ~38% annualized).

The setup is still defensible but the timing is off. The flow tells you institutions are positioned for more downside in the next 17 days, and IV is going to stay elevated through that window. If you sell that put today, you're stepping in front of a freight train that hasn't finished arriving.

Three better ways to play it:

- Wait 1 week. Let the May 15 puts work or fail. If RMBS holds $105-$110 by next Tuesday, IV crushes, and the bearish flow gets faded — that's your green light to sell the June $95P at probably $4.00-$4.50, lower premium but cleaner setup.

- Roll out, not down. Sell the $95P 08/21/26 (115d) instead. Premium is fatter (closer to $7-8 likely given current IV), gives you a full quarter for the dust to settle, and makes assignment easier to manage. Annualized return is similar but you're not paying the gamma tax.

- Convert to a put credit spread. Sell $95P / Buy $80P 06/18/26. Caps your risk if RMBS goes to $70 (which the flow suggests is on the table), keeps roughly 60-70% of the credit. You give up the wheel mechanic but define the risk during a period where institutions are clearly hedging for more downside.

Bottom Line

This isn't ACLX (broken thesis from misread setup). RMBS is a real wheel candidate — the AI memory thesis is intact, multiple Wall Street firms still have Buys, and you'd own it at $95 if assigned. But the flow says don't sell that put today. Wait for the institutional bearish positioning to play through, or move out to August expiry to absorb the volatility. The $60+ run from $80 to $158 doesn't fully reset in one day — there's likely another leg lower or a multi-week base before this stabilizes.

If you want to act tonight, the August $95P is the cleanest version. The June $95P at the screen's $5.05 is "fine" — but you can do better with a week of patience.